Financial goals are objectives that you want to achieve with your money. They help you to control where your money goes and what you do with it. These goals can be broken down into the length of time it will take to achieve them: short-term goals (less than one year), mid-term goals (2-5 years) and long-term goals (five years or more).

Why is it Important to Set Financial Goals?

It’s important to set financial goals to ensure that you have good financial health throughout your life. These goals help you to be more intentional with your money. That means they guide your decisions when it comes to how you handle your money (i.e.: save it, invest it, spend it).

Let’s use an example to explain this point. Perhaps you’ve seen financial advice that says to skip buying coffee everyday and make it yourself instead. But you really enjoy that coffee from Starbucks – it’s so delicious. You want that enjoyment and it’s only $5, so you ignore the advice. What’s the big deal anyways?

Well, if you typically buy a coffee every work day, that $5 per coffee turns into $100 a month! At the same time, you really want to go on a summer vacation. But it’s going to cost you $1,000 – and you don’t have an extra $1,000 in your savings account.

Then you hear about this thing called setting financial goals, so you set saving up for that summer vacation as one of your goals. As you go through the steps outlined below, you realize that the best way to save is to reduce your Starbucks coffee from 5 days a week to 1 day a week. Bingo! Goal accomplished.

That’s the power of setting SMART financial goals. Are you ready to learn how this process works?

How to Set Realistic Financial Goals

Have you ever set a goal and then didn’t meet it? It’s frustrating, disappointing and maybe those feelings even led you to quit trying. But don’t stop trying … there is a better way!

How? The best way to reach your financial goals is to set SMART goals. What does SMART stand for and what does it mean? SMART can be broken down as follows:

- Specific – Set detailed and clear goals.

- Measurable –Track and measure your progress.

- Achievable – List action steps to meet your goals.

- Relevant – Remember why your goal is important to you.

- Time Bound – Give your goals a deadline.

I’ll get into each one of these steps below in more details. Then, as you go through them, sum up your answers in a one-page plan. This plan will incorporate all 5 aspects of SMART goals.

Before we go any further, I want to clarify two points:

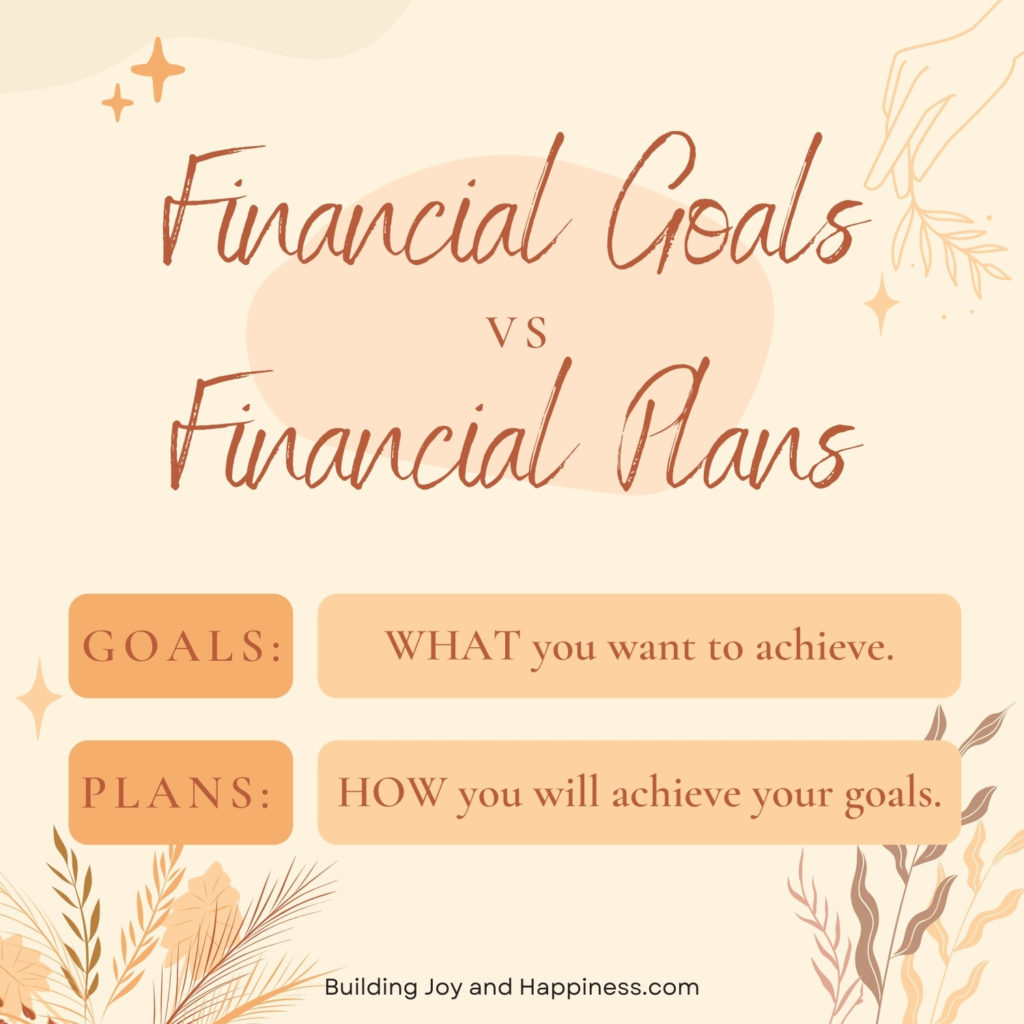

- Financial GOALS are WHAT you want to achieve.

- Financial PLANS are HOW you will achieve your goals.

That’s the beauty of SMART goals – they’re not just random goals that you hope you can accomplish. They’re goals that you know you CAN achieve, WHEN you will achieve them and HOW you will do it.

Specific: Set Detailed and Clear Goals

The first step is to determine WHAT your financial goals are. I talked about setting financial goals in two previous posts. Take a moment to review these posts (listed below) and write down which goals you would like to adopt. Keep in mind that you can have a long list of goals, but you can prioritize your list and work on only a few at a time. I get into this a bit more in the T (Time Bound) section below.

- 11 Examples of Short-Term Financial Goals for Women to Adopt.

- 11 of the Most Popular Mid and Long-Term Financial Goals.

Once you have a list of your goals, write up a quick one-page summary for each goal. Remember, these goals need to be detailed and clear. That means you need to add lots of details. For example, if you are saving for a car, in addition to the amount you will need, write down the make and model of the car you want. The clearer your goal, the easier it will be to stay motivated.

“Knowing your values can make it easy to say no to things that distract us from what’s most important”

Carl Richards, author of “One Page Financial Plan”

Measurable: Track and Measure Your Progress

Setting goals is a good first step. But if you aren’t measuring or tracking your progress, how will you know when you have reached your goal? It’s also why you took time to add lots of details to your goals in the step above.

Let’s use the example of saving for a car. Now that you know the amount you need, you can determine the amount you will need to put aside each month. As long as you are putting aside that amount, you know you’re on track.

If you need to, keep the money in a separate account. If that account also contains money put aside for other items, keep a spreadsheet that breaks down the total. For example, you have a separate savings account with a total of $3,000, which can be broken down into:

- Emergency fund = $2,000

- Car fund = $700

- Christmas presents fund = $300

Achievable: List Action Steps to Take

For any goal to be reached, it needs to be achievable. I can set a goal of buying a $10 million dollar house next year, but if I’m making $100k/year, it’s probably not going to happen. Sigh…

So, always ask yourself:

- Is my goal realistic?

- How can I accomplish it?

Question #1: Is my goal realistic? Remember to take into account your current and expected future circumstances. Wait – how can anyone know the future? While there are a lot of unknowns, you do have some idea of your plans. For example, if you are planning on having children, you will have to allow for reduced income while you are on mat leave and after that, you have to allow for the added expense of daycare.

Question #2: How can I accomplish it? List ways and action steps that you will take to meet your goal. One tool that can help you with this step is to create and follow a budget. I personally love following a Zero-Based Budget! This budgeting method allocates all of my income to a purpose: saving, debt repayment or spending. It allows me to create a mindset of being INTENTIONAL with my money!

Relevant: Why is your goal important to you?

In life, things will happen. There will be unexpected expenses or other desires you will have. It can throw your financial goals off progress. That’s why it is necessary to write down why each goal is important to you – this will help keep you focused and motivated to reach your goals.

Write down not only why it’s important, but how accomplishing this goal will make you feel and what benefits will it bring you. The key here is to have an emotional link to your goal. For example, you could write, “Being debt free gives me the flexibility to leave my job, even if the next job is lower paying. It is more important to be in a work place where I feel appreciated and be engaged in my work.”

TIP: If you are looking to reduce spending, try reframing each purchase. Before you buy something, ask yourself two questions:

- Do I really need this?

- If I spend my money on this purchase, it’s taking that money away from my financial goal(s). Is this purchase worth delaying my financial goals?

Time Bound: Give Your Goals a Deadline

For each goal, include your deadline for achieving that goal. Don’t worry about getting this perfect or making a mistake – you are allowed to change the deadline. But it does need to be a reasonable time frame. Too short and you won’t be able to meet your goal. Too long and you might not feel like you’re making enough progress.

The benefit of a deadline is that it forces you to prioritize your goals and how you handle your money overall. For example, you could set 10 goals and start working on all of them at once – but end up feeling like you’ll never reach any of your goals. Or, you could prioritize your goals and put them in order of importance to you. As you complete one goal, you then start working on your next goal. This method allows you to feel a sense of accomplishment as you successfully meet one goal after another!

Final Thoughts

Once you have set your goals, don’t forget about them. An important part of meeting goals is to regularly see how you are progressing (that’s the “M” in SMART)! If you’re not on track, go through your finances to find out why and then figure out what you can do to get back on track.

Finally, when setting goals, it’s important to remember to review and revise them any time there are changes in your life. This could include changes you control, such as having a child, OR changes you can’t control, such as expenses increasing due to inflation. That’s life – things happen. Find the good in where you are, accept what you cannot change and make it work for you.

Until my next blog post, here’s wishing you lots of joy and happiness!

With love,

{kind=link}

Very enlightening for newbies in finance management. I loved how you practically explained about achieving financial goals.

Great piece. When thinking about long-term savings goals it can be overwhelming. Setting small, achievable steps is the best way to get on track and build your savings. It is also encouraging as you see small goals being met and your savings begin to grow.