So, you probably already know you should be saving money. And maybe you’re already pretty good at putting money aside. But now it’s time to take that saving one step further – through the use of something called “sinking funds”. Probably about now, you’re asking yourself, “What’s that?”. Don’t worry. I’ll go through exactly what sinking funds are all about, the benefits and how to set them up. Ready? Let’s go!

What are “Sinking Funds”?

A sinking fund is a specific amount of money that you save each month. This money will be used for a specific purpose (like a vacation) or for expenses (like car repairs), that you know you will have in the future. These funds help you to be intentional with your money and how you use it.

The Benefits of Sinking Funds

So, maybe you already have a savings account and put money into it. Or, you only have a main bank account and you have enough money in it to avoid living paycheck to paycheck. Excellent! If so, you may be asking why you need to set up a sinking fund. Well, there are many benefits of sinking funds, including:

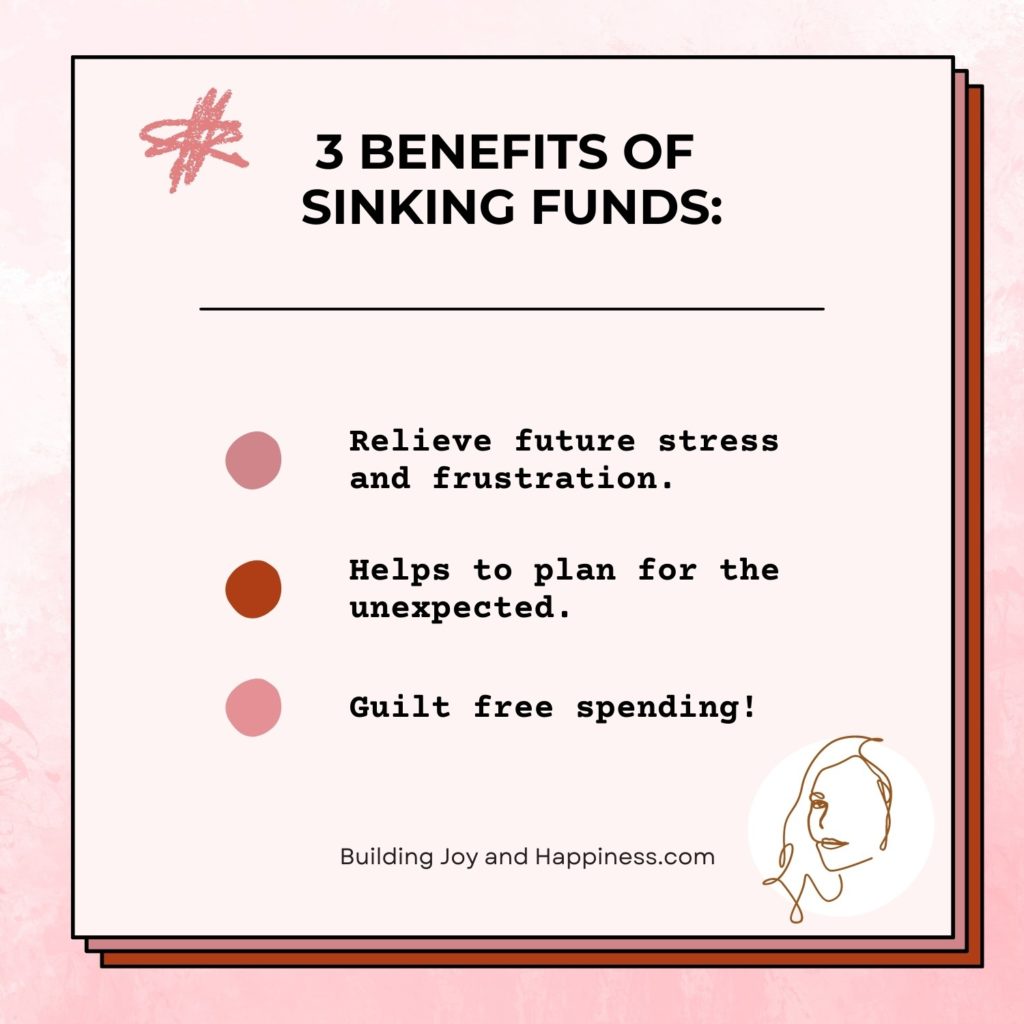

- Relieve future stress and frustration. How? When the expense does occur, you are not forced to use up general savings or go into debt.

- Plan for the unexpected. Like what? You know certain expenses will happen, but maybe not exactly when (like new appliances or house repairs).

- Guilt free spending! Set up a sinking fund for fun things (like a vacation). As long as you don’t spend more than you have saved, you don’t have to worry about spending the money.

How to Create a Sinking Fund

Here’s a quick overview of how to create a sinking fund. I’ll go into more detail for each step below.

- Decide what you want to save for.

- Decide where you will keep the funds – in a separate account or in your main bank account.

- Decide how much you need to save for each fund.

- Determine how long you will need to save.

- Calculate your monthly contribution.

- Include your monthly contributions in your budget!

Step One: Determine Your Sinking Fund Goals

Before you start saving money, you need to figure out what you want to save for. Here are some items that you may wish to adopt in your sinking fund list:

- Emergency fund,

- Vehicle repairs,

- House repairs,

- Annual property taxes,

- Birthday parties and gifts,

- Christmas presents,

- Save for your wedding,

- Save for a vacation,

- Tuition fees,

- Vet bills,

- Annual subscription renewals,

- Seasonal clothing,

- Save for a new car, and/or

- Save for new appliances.

As you can see, some of these items are short term (less than one year) and some can have a longer timeline. Some items are for necessities (for example: taxes, annual bills, etc), however, sinking funds can also be used to save up for fun things (like vacations and birthdays).

Step Two: Decide Where to Keep Your Sinking Funds

There’s no right or wrong place to keep your sinking funds. Ideally, it should be a separate account, so that you don’t accidently use the funds for something else. Also, you should be able to access the funds quickly and without any additional fees. The reason is that this is money you will be probably be using several times throughout the year, depending on what you want to use your sinking funds for.

Finally, it’s perfectly acceptable to keep your funds all in the same account (but a separate account from your main bank account). The main advantage of having one account, is that it reduces paperwork and the need to keep track of so many different accounts. Plus, with the help of a sinking fund tracker (see my Etsy shop for trackers that you can easily customize to your needs), it’s easy to keep track of how much money you have saved for each different purpose.

Step Three: Decide How Much to Save

So, you’ve decided which items you want to save for. Excellent! But how do you determine how much you need to save?

Well, for many items, it will be easy to determine what your goal amount is. For example:

- You can research what the item will cost (i.e.: car repairs will include oil changes every 4 months), OR

- You can set an amount that you feel comfortable spending (i.e.: for Christmas presents, you can make a list of people and how much you wish to spend on each person).

However, for some items you know it will happen in the future, but not the exact amount. For example, your car is getting older and it will most likely require more repairs. So, how much should you save? Here are 2 methods to choose from to help you determine the amount:

- You can base the amount from an average of previous car repairs, OR

- You can research common car repairs and how much they cost. Then, take the average of these costs and set that as your goal.

Step Four: Determine the Length of Time Needed to Save

So, now that you know how much you want to save, you need to figure out how long it will take you to save that amount. For many items you will know when the expense/purchase will occur. These are more likely to be recurring expenses or events.

However, for other items, while you know they WILL happen, you don’t know WHEN. In those cases, how do you set an ending date? In these cases, do some research and make a reasonable estimate. Even if the item happens sooner than expected, at least you will have some savings for it. For example, you know you will have to replace appliances in the future. Based on a Google search, you find out that the average life for appliances is 10 years. Go ahead and use 10 years from now as your ending date.

Step Five: Calculate Your Monthly Contribution

This is the easiest of all the steps you will follow when setting up your sinking funds. Simply take your goal amount and divide it by the length of time to save. Let’s take an example of saving up for Christmas presents. You have decided that you want to save $550 over the next 11 months. That means you need to save $50 every month to meet your goal. Expressed as a mathematical formula, your calculation will be: $550/11 months = $50/month.

Note: Feel free to change the time from months to weeks or every 2 weeks. The way you do the calculation will be the same.

Step Six: Include Your Sinking Fund Contributions in Your Budget

Setting up your sinking funds is only the start. The final step, is to make sure that you are actually saving that money! A good way to do this is by including your contributions in your budget. One benefit of putting this total in your budget, is that you will be able to see if you can afford to save that amount each month.

But what should you do if you can’t afford the total of all the contributions you just calculated in step five? Here are three suggestions:

- You could look for a lower cost option. Yes, a big trip that requires flights, a car rental AND a hotel would be amazing. But perhaps a vacation closer to home – one where you only need to pay for the hotel costs – would still be a great vacation!

- You could set a longer period of time, which will give you more time to save the money needed. If you choose to go for this option, just make sure that the time period is reasonable. If you have to save for a yearly expense, it won’t make sense to stretch the time period out for longer than a year.

- Focus on priorities. Sometimes, you just can’t do everything and you need to focus on saving for the most important things first. Plus, if you are trying to save for too many things at once, you won’t feel like you are making any progress.

There’s one more thing that I would like to point out. If you have debt, other than a mortgage, you should concentrate on first creating an emergency fund of $1,000. Next, put all of your extra money to debt repayment, until it is finally paid off. Then, you can look to fully build up your emergency fund and create other sinking funds. Why? That’s because this method will help you save LOTS of money from the interest charges on your debt. Over the long run, that will help you reach all of your financial goals quicker.

Leave a comment below and let me know what strategies you use to either calculate your sinking funds OR what strategies you follow in order to put money into your sinking funds.

Until my next blog post, here’s wishing you lots of joy and happiness!

With love,

{kind=link}